The information contained in this article is not intended as legal advice and may no longer be accurate due to changes in the law. Consult NHMA's legal services or your municipal attorney.

“Forecasting is very difficult, especially if it is about the future.” –Niels Bohr, Nobel Prize-Winning Physicist

Forecasting revenues is a fundamental part of budgeting and financial planning. Revenue forecasts allow public officials to anticipate resource availability and plan accordingly for things like enhancing services to the community, changing the salaries and benefits of public employees, and adjusting tax rates. Governments use 12- to 18-month forecasts to develop budgets that are balanced and affordable. They use longer-term forecasts to analyze the financial sustainability of existing policies and programs, and to provide warning about potential imbalances in the government’s financial future. A forecast provides a shared basis for discussion about what the fiscal future might look like and what actions can be taken. In the absence of a formal forecast, a common assumption is that the future will not be much different than the past – an assumption that could be seriously flawed.

That said, to paraphrase Niels Bohr, forecasting is not without its challenges. One of the biggest challenges is that forecasts are often not effective in influencing financial decisions. Frequently, decision makers are much more strongly influenced by other factors. A forecast is not effective at influencing decisions just by virtue of its accuracy and reliability. These elements are necessary and important, but alone they are not sufficiently effective. This article examines several strategies you can use to boost the utility of your forecast.

FORECASTER CREDIBILITY

Establishing the forecaster’s credibility is essential because decision makers are more likely to use a forecast from a trustworthy source (and less likely to use a forecast from a disreputable source). Therefore, a good place to boost the utility of your forecast is to build credibility. Even if you don’t have a credibility problem, more credibility is never a bad thing. In any case, research suggests that people generally overestimate how trustworthy and credible they seem to other people.

Understand Your Audience. A forecaster who demonstrates an understanding of the audience’s concerns and needs will seem more credible. Common questions about a revenue forecast might include: What are the implications for constituents’ tax bills? Can we lower taxes? What is the impact on high-priority (often capital) projects? Can we afford improvements or augmentations to a high-priority service? Are our current services and obligations affordable into the future?

One way to cement an understanding of the audience’s concerns is to discuss them directly. For example, in the City of Sunnyvale, California, staff met with elected officials to review the city’s long-term forecasts in study sessions, rather than the regular council meetings. This allowed the elected officials to ask questions and exchange ideas with staff about key forecast assumptions before it was presented at the city’s council meetings. Staff was then able to fine-tune the forecast presentation, which A) better aligned the forecast presentation to the informational needs of elected officials, and B) demonstrated to elected officials that staff took their questions and concerns seriously. For example, elected officials were often curious about how new growth and development projects would affect the city’s tax revenues. The informal meetings gave the council and staff the opportunity to discuss the point at which new development would be included in the forecasts versus when it was too speculative to be included. Because there were differences of opinion on this question, the less formal meetings allowed for a more relaxed discussion than might have been possible in regular council meetings.

Know the Facts. Having a substantive command of the facts underlying revenue performance builds the forecaster’s credibility. The details a forecaster should know will depend on the community. For example, the City of Palo Alto, California, has a population of about 66,000 and is located at the epicenter of Silicon Valley. Palo Alto’s staff remains abreast of the health in the Silicon Valley economy in general, and growth in venture capital activity in particular because those measures have been reliable indicators of the economic activities that will affect Palo Alto’s revenue sources. Palo Alto also pays close attention to microeconomic statistics. For instance, one of the city’s revenue sources is a tax on hotel occupancy, so it monitors room rates, occupancy rates, and the construction of new rooms.

The City of Houston, Texas, is the fourth-largest city in the United States, so it wouldn’t be practical for Houston’s forecasters to achieve the level of granularity that a smaller government like Palo Alto might need. However, Houston does conduct detailed examinations of key industries in the local economy like oil and gas, as well as other indicators of economic performance that foreshadow revenue yields. As a result, though Houston’s staff may not have the same level of detail as a smaller city, they can still credibly demonstrate their knowledge of the environment.

The forecaster should translate a strong knowledge of the environment into a set of assumptions about the financial and economic environment that underlay the forecast. The assumptions should rely on objective information that is relevant to the factors that drive revenue yield. To the extent possible, the assumptions should also be compared to forecasts or analysis performed by credible third-party experts such as consultants or universities. Differences may increase credibility if there are clear local circumstances that merit a difference from regional trends – this shows the forecaster’s knowledge of the environment. If a third party’s analysis is directly relevant to the circumstances of the forecaster’s organization, then similarities between assumptions can also increase credibility, as the forecaster is thus shown to not have biases that cause him or her to deviate from what other analysts examining a similar question have found.

Acknowledge Uncertainty. A forecaster can maintain credibility while acknowledging uncertainty around the assumptions. In fact, acknowledging uncertainty can strengthen the forecast. The forecaster for the City of Manhattan, Kansas, labels particularly uncertain assumptions “wild cards” and demonstrates for the audience how different outcomes in the wild-card assumptions could raise or reduce city revenue. This helps decision makers prepare for outcomes that differ from the baseline forecast.

Decide If You Want to Adopt a Conservative Approach. One of the toughest issues in maintaining credibility as a forecaster is making “conservative” versus “objective” forecasts. A conservative forecast systematically underestimates revenues in order to reduce the danger of budgeting more spending than actual revenues prove able to support. An objective forecast seeks to estimate revenues as accurately as possible, with the goal of making optimal use of all available resources—but it also carries a higher risk of being too optimistic (which could lead to budgetary shortfalls during the fiscal year). Governments with highly effective forecasts are almost evenly split in describing their forecasting approaches as objective or conservative, with a slight tilt toward “objective,” on the whole. While these governments had two different philosophies among these governments, there was one important commonality: The decision to be objective or conservative was explicit and consistent with the goals and expectations of the governing board.

For example, in the case of the conservative forecasters, the governing boards have a clear preference for end-of-year surpluses that could be put toward building reserves or paying for capital projects. There is an expectation, then, that actual revenues will exceed what was budgeted, so when they do, no one is shocked or disappointed and the forecaster maintains credibility. However, for governments where the board does not have this same preference, a conservative forecast could lead to credibility problems. If actual revenues consistently exceed forecasts, decision makers may come to feel that the forecaster is unreliable or, at worst, manipulative. In recent years, one government that experienced this challenge has moved toward more objective forecasts to be in line with the preferences of the governing board. Before that, when the finance staff produced conservative forecasts, some board members felt that that the finance office was “playing games” with the budget.

Of course, an objective forecast could also harm a forecaster’s credibility, especially if the forecast is too high and the government is forced make painful budget cuts. Governments with effective forecasts and an objective forecast philosophy adopt a number of strategies to mitigate the risk posed by shortfalls (e.g., contingency accounts, short-term revenue monitoring, etc.) and maintain credibility.

IMPLEMENT PRINCIPLES AND PROCESSES THAT SUPPORT THE USE OF FORECASTING

Forecasts will be more effective at influencing decisions if they are inputs into a decision-making process that encourages good use of forecasting information. Policies that emphasize the fundamental principles of financial health, such as minimum reserve levels and appropriate use of one-time revenues, set the tone for using forecasts in decisions.

Developing Principles. Financial policies have been a mainstay GFOA best practice for years; however, a less well-known practice is that of financial principles. Principles bridge the gap between the rationality of a forecast and the emotions that often drive decisions. Principles speak to decision makers’ passions and values by asking them to answer questions like “What kind of organization do we want to be?” and “What kind of leader do I want to be?” For example, Traverse City Area Public Schools (TCAPS), in Michigan, adopted three principles to guide its decision making:

- Education priorities should drive the budget. The TCAPS budget should reflect the most current strategies for providing a world-class education to its learners. The budget should not just be an incremental adjustment from whatever was done last year.

- You can’t be all things to all people. Delivering world-class education at an affordable cost demands focus. TCAPS should pursue a limited number of specific goals.

- There should be a focus on academic return on investment—TCAPS should get the most bang for its buck.

Such principles help decision makers put a higher value on financial analysis than might otherwise be the case. For example, if TCAPS is to actively seek out the best strategies for educating its learners, and break with past practices when necessary, then it needs a forecast to better illuminate the path forward. In fact, TCAPS’ board has used its principles as the basis for financially savvy decisions such as selecting programs based on cost-effectiveness and optimizing the size and scale of school buildings based on enrollment.

Considering the Budget Process. Though principles and policies help create a mindset that includes forecasts in decision making, the most important financial decisions are made during the budget process. The budget process, then, must be designed to encourage the use of forecasting information. The foremost design principle is that non-traditional budgeting formats tend to encourage better use of forecasting. Traditional budgeting formats are characterized by an emphasis on control of spending through detailed line items; the inputs into public services (i.e., staffing, materials, etc.) rather than the outcomes; and incremental decision making, wherein the government starts the budget with last year’s expenditures and adjusts them up or down at the margins as may be required, given assumed revenue growth or contraction. Conversely, governments with budgets that incorporate a planning orientation, take program performance into account when allocating resources, and take an explicit, structured approach to weighing competing potential uses of resources against each other are more likely to get value out of revenue forecasts.

A good example of how a less traditional approach can encourage better use for forecasting information is the beginning of the budget process. The traditional, incremental budget process tends to emphasize expenditures because budget discussions begin with the question, “What did we spend last year?” An alternative approach to budgeting starts by asking what resources are available, perhaps engaging public officials to have a discussion on whether tax and fee levels are appropriate given the service demands of the public. This difference in approach, although subtle, emphasizes revenue forecasts as a tool to reveal the level of resources available as the starting point for budget discussions. The City of Auburn, Alabama, describes this as a “live within our means” philosophy that has been important for focusing their decision makers on the forecast.

Beyond annual budgeting is long-term financial planning and visioning. Long-term financial planning has become increasingly common among leading local government budget practitioners. A GFOA survey of leading budget practitioners found that 59 percent of respondents had implemented a comprehensive planning process (with some having started as early as 2008). Critically, the vast majority of these (90 percent) believe that multi-year financial planning and projections have improved fiscal discipline and long-term financial sustainability in their governments, and two-thirds of those described the improvement as significant.

DEVELOP AN ACCESSIBLE PRESENTATION FOR YOUR FORECAST

It is not easy for a forecaster to get his or her message across in a way that will stay with those who hear it. Finance will not be the first language of many audience members. Even those with more financial expertise will likely not have the same breadth and depth of experience with revenue analysis as the forecaster, so they may miss some nuance. These challenges mean that the forecaster must be careful to present forecast information in a way that maximizes its accessibility.

Getting the forecasting message across starts with a clear understanding of what the audience needs and wants to know. Even if the message is focused on the essentials, a problem is that local government revenues are often measured in sums that the audience has no practical, real-life experience with; they do not have access to millions of dollars in their personal lives, so the forecast numbers are an abstraction to them. Therefore, the forecaster needs to make the numbers more fathomable. The most basic way of doing this is by comparing revenues to expenditures and reserve levels, thereby making the connection between the revenue forecast and the prospects for achieving and maintaining structural balance in the budget. It also suggests, for example, the implications for tax rates, a city’s ability to put a certain number of police officers on the streets, or a school district’s ability to put a certain number of teachers in classrooms.

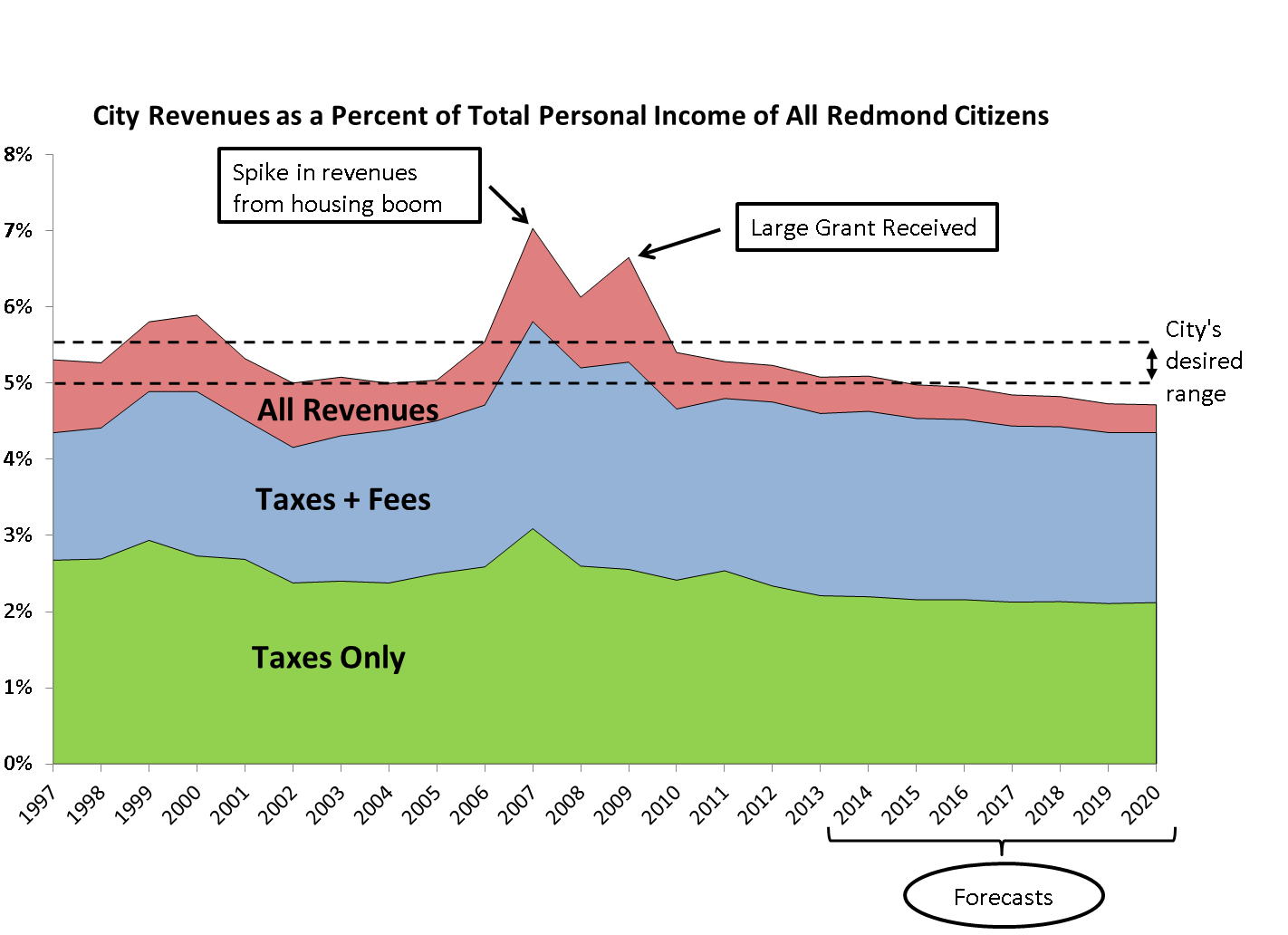

Another powerful way to make forecast numbers more tangible is by reducing numbers to a personal scale, such as showing revenues per capita (e.g., per resident or per student) or showing the impact of revenue changes on individual tax bills. Fairfax County, Virginia, shows a five-year history of the property tax on a typical homeowner, using the average assessed value of a home in the county. This shows the impact of any changes in revenue on the taxes paid by a homeowner. The City of Redmond, Washington, has used a method called “the price of government” with success. (See Exhibit 1.) It compares the city’s revenues against the total personal income of all Redmond residents, revealing how much of citizens’ resources are being consumed by the city and providing a good context for city council discussions about what increasing or decreasing revenues would mean for constituents. (Total personal income for the community is calculated by multiplying Redmond’s per capita income from the U.S. Census Bureau’s “American Community Survey” by the city’s total population. While this does not capture income from Redmond’s commercial sector, the city still finds it a useful proxy.)

Exhibit 1: The City of Redmond’s Price of Government Presentation

{kind=link}

A powerful way of making forecast numbers more concrete is to use interactive forecasts to simulate changes in key variables or forecast assumptions. Excel (and other software packages) can be used for graphical what-if analyses with variables that change live, in front of the audience, allowing them to see the effects of the change for themselves. Research shows that such interactivity enhances the audience’s understanding and retention of numbers because the audience is able to engage with the presentation, rather than sit back as passive observers.

Finally, know that the speaker’s confidence level has a powerful impact on the believability of his or her message. The term “con man” is a modern shortening of an older term, “confidence man” – a powerful, if disturbing, demonstration of the power of confidence to make a message believable! While forecasters should certainly not seek to “con” the audience, they must be aware of the effect that their perceived level of confidence will have on the way in which the message is received. A balance must be struck between presenting the forecast with its inescapable uncertainties and projecting the confidence that comes from having performed a thorough technical analysis with strategies that mitigate risk.

CONCLUSIONS

Because decision makers are strongly influenced by factors other than facts, a forecast itself will not make effective impact decisions just because it is accurate and reliable—they are necessary but not sufficient. But several strategies are available to help you improve the utility of your forecast. Improve your credibility by understanding your audience, knowing the facts, acknowledging uncertainty, deciding on a conservative or an objective” forecast. Implement principles and processes that support the use of forecasting. Develop principles and consider the budget process. And finally, make your forecast accessible.

SHAYNE KAVANAGH is the Senior Manager of Research for GFOA’s Research and Consulting Center. He can be contacted at skavanagh@gfoa.org. This article originally appeared in the February 2017 issue of Government Finance Review (www.gfoa.org) and is adapted from Informed Decision-Making through Forecasting: A Practitioner’s Guide to Government Revenue Analysis, by Shayne Kavanagh and Daniel Williams (GFOA: 2017).